I recently had to place a small business owner in a 27-percent annual-rate cash advance loan. The sad thing about his situation is that he might well have been eligible for a six percent bank loan. What stood in his way was that he was six months behind in his bookkeeping, and it would take two weeks for him to get his books in order.

Unfortunately, he needed the money right away. And there isn't a reasonably priced lender out there who will lend to anyone with such outdated financials. It's easy to look at this situation and think that the owner got what he deserved. But the reality is that it's easy to slip on keeping up the books. I am guilty of it sometimes, too. When I get lazy, I keep an eye on the bank statement to make sure cash is coming out, and I save the bookkeeping for later.

I was reflecting on this recently, as I watched my 12-year-old son play basketball. While I confess to not understanding much about the game, I love the intensity, and I love watching how he has grown and changed as a player over the years. And I see similarities between being a basketball player and an entrepreneur.

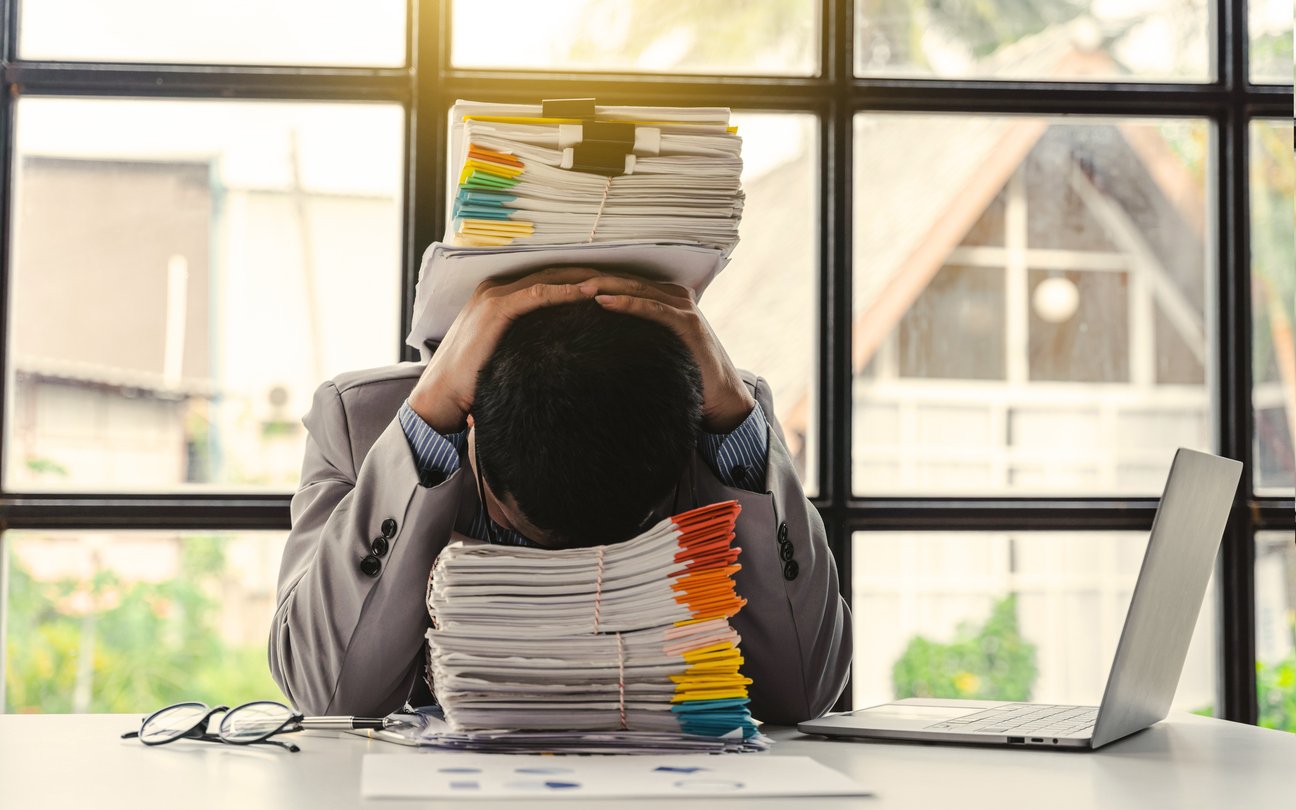

Perhaps most striking is how quickly you have to flip between playing offense and defense. At any moment, everything can change. In basketball, you wouldn't try to get on the court if your shoes were untied. And in business, you really can't play the game unless you have a core understanding of your financials and cash flow. Unfortunately, many small-business owners are so focused on their trade that they don't give sufficient time or attention to their books.

And then the unexpected happens. Suddenly, you are playing defense, and you need those financial statements. If you are unprepared, it's as bad as being on the basketball court with untied shoes. Every day, at my loan brokerage, we get phone calls from business owners who are dealing with something new and want to look into a loan for help. The state of their financial statements will often dictate what options are available and what rate they will have to pay.

The issue of outdated bookkeeping is particularly important at this time of year, when we see many clients who are in the process of compiling their receipts and bank statements for the previous year so their accountants can prepare their tax returns.

By Ami Kassar, The New York Times.